ACCM4200 Advanced Financial Accounting Report

Assume that you are a team of graduate accountants working for Kaplan Pty Ltd, an independent consulting & accounting firm located at 63 Elizabeth Street, Sydney, NSW 2000. Among other things, your firm provides its clients with advice regarding accounting issues, including applying the Australian Accounting Standards in preparing Financial Reports. You must prepare a Statement of Advice (SoA) for National Ltd to address several accounting issues raised by Ms. Kathy King on behalf of the company's directors. Ms. King has raised these issues in a letter in the following pages.

The maximum length for the SoA is 2,000 words (+/- 10%). You should address all the technical issues in your advice, followed by a Reference List. Marks will be awarded based on two components:

Technical component 30% - This includes the technical discussion in your SoA, the explanation of each issue, and the sources used. You must analyse the information provided and recommend the correct accounting treatment. You must justify your recommendations by referencing specific paragraphs of relevant accounting standards. You must explain the rationale behind each accounting standard requirement. Communication Skills (Writing Skills) component 10% - marks will be awarded based on your ability to gather information and effectively communicate strategies to the client as part of the SoA. It will also cover the generic skill of writing, clear meaning, structure and organisation, appropriate tone and grammar, spelling, and punctuation, etc., throughout the whole assignment.

Please provide some recommendation on the following issues with appropriate accounting treatments as per the Australian Accounting Standard.

1) As at the beginning of the current financial year 2024, High Ltd has two provision accounts:

(a) Provision for lawsuit claims $14m, and

(b) Provision for warranty $29m.

During the year ended 30 June 2024, the lawsuit claims were settled at $16m and warranty costs of $32m were paid. We would like to increase the warranty provision to $39m at year end in tandem with the increase in products sold during the year.

Please provide journal entries (if any) that we should make for 30 June 2024 to prepare our annual report. Please show all workings (settlement of the lawsuit claims and increase of warranty provision).

2) High Ltd is the primary contractor responsible for constructing a power plant for Thai Lid. It has been discovered that there are defects in the construction of the power plant. The estimated cost to fix these defects is $100m. It had previously recognised a provision for warranty of $40m on the project as part of project costs. However, High Ltd believes it can recover a substantial part of the costs from the subcontractors who performed some of the construction works. Negotiations with these subcontractors are ongoing, and so far, only two subcontractors have accepted liability. The amount of reimbursement that is considered virtually certain is estimated to be $10m.

Can you explain with journal entries how High Ltd shall account for the above estimates of costs and reimbursements? What would be criteria for recording such liabilities?

3) The ice cream factory located in Thailand has been incurring losses for the past 3 years.

Management is contemplating the option of either restructuring the plant or selling it to an external party. Management believes that losses will continue for another 2 years at about $30m per year before the business operation could turnaround. At year end, neither the restructuring plan nor the plan to sell was finalised. The carrying amount of the net assets of the plant at year end was $400m. Based on its current condition, the recoverable amount of the plant was estimated at $350m. Can you explain the accounting treatment that shall be accorded to the above case, shall we record provision liabilities?

4) On 18 March 2024, the Board of Directors of the company decided to close down the chocolate making products plant. On 25 May 2024, a detailed plan for closing down the plant was agreed by the Board; letters were sent to customers warning them to seek an alternative source of supply and redundancy notices were sent to the staff of the plant. The carrying amount of the net assets of the plant is $20m. The net proceeds from selling the individual assets and settling the liabilities is $12m.

Other costs expected to be incurred are as follows.

• termination costs of $2m (changes in management structure costs),

• costs to sell a line of business $3m,

• staff relocation costs $1.2m,

• staff retraining costs $1.4m and

• expected additional operating costs for the first quarter of 2025 financial year $8m.

The closure of the plant is expected to be completed by 25 August 2024. The company's year- end is 30 June. Can you please explain, with reasons, whether the closure of the plant shall be recognised in the financial statements of 2024. Also, state the amount of provision, if any, which shall be recognised in its financial statements.

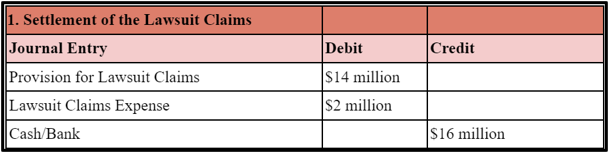

A consensual settlement that finalises a disagreement and causes any pending litigation to be dropped. Parties often decide to keep their settlement agreements confidential, regardless of the specific provisions (Thathoba, 2023). In terms of preparing journal entries regarding this settlement of the lawsuit claims and adjustment of the warranty provision (Refer to case study). There is a need to account for the settlement of the lawsuit claims, payment of warranty cost and adjustment of the warranty provision to reflect the increment of $39 million in the end year.

At the beginning of the financial year, a provision of $14 million was made for lawsuit claims. Here, need to record both the payment and the additional expense here because the actual settlement cost was $16 million.

Table F: Journal entry for Settlement of the Lawsuit Claims

(Source: Author)

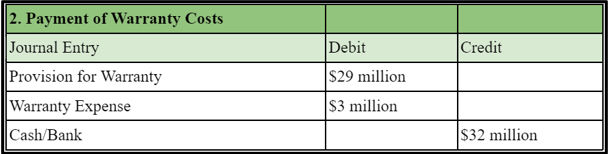

Payment of Warranty Costs

There was a provision for guarantee of $29 million at the start of the financial year. Last year, repair costs came to $32 million.

Table G: Journal entry for Payment of Warranty Costs

(Source: Author)

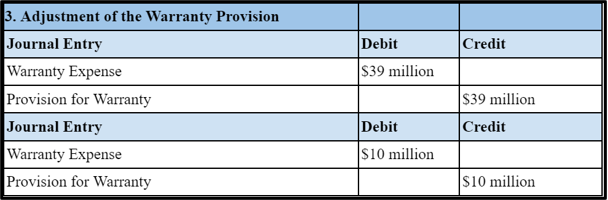

Adjustment of the Warranty Provision

This review had to modify the provision for MBA assignment expert promise in order to account for the increase to $39 million at the end of the year. There is only one more increase to show here, though: $39 million. It had a provision of $29 million at the beginning of the year. After paying for costs, it needs an additional $10 million to reach $39 million.

Table H: Adjustment of the Warranty Provision

(Source: Author)

Issue

The settlement entails appropriately accounting for lawsuit costs, warranty costs, and guarantee provision modification (Kartapanis and Yust, 2024). The original provision for the lawsuit claims settlement was $14 million, but the ultimate settlement cost $16 million, requiring an additional $2 million expense. Because the original provision of $29 million fell short of the actual $32 million repair costs, an additional $3 million provision was required for guarantee costs (Refer to case study). By the end of the year, the service provision had climbed from $29 million to $39 million, requiring an additional $10 million provision adjustment. All of these adjustments must be recorded in paper notes for accurate financial records.

Accounting treatments

Based on the facts provided, changes must be made to the lawsuit costs, service costs, and promise terms. The original $14 million provision for lawsuit claims was raised to $16 million, generating a $2 million additional expense (Even-Tov, 2024). The initial $29 million warranty provision was inadequate for $32 million in repair costs, requiring an additional $3 million (Christensen, 2024). By year's end, service provision rose from $29 million to $39 million, requiring $10 million in changes (AASB Standard, 2018). These adjustments should be properly documented as expenses and reserves and explained in the financial records, per AASB standards.

As per AASB standards the following section develops to estimate the cost and reimbursement in terms of the defects within the power plant construction regarding High Ltd (AASB Standard, 2018).

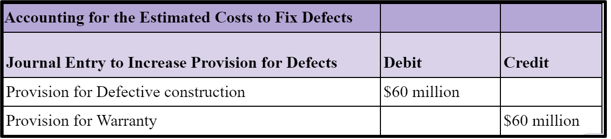

Accounting for the Estimated Costs to Fix Defects

According to High Ltd., the costs to fix the defects in the power plant construction will probably come to $100 million. Before the project began, they were aware of a security provision of $40 million.

Table I: Adjustment of the Warranty Provision

(Source: Author)

The Provision for Defective Construction is made to account for the anticipated costs ($100,000,000) to fix the defects. The current provision for a guarantee of $40 million is being reclassified and raised to cover a wider range of costs related to the defects.

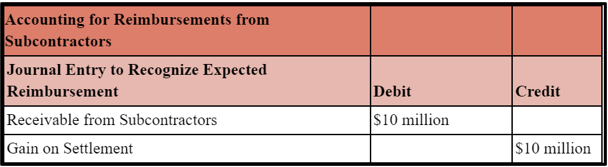

Accounting for Reimbursements from Subcontractors

High Ltd. expects to recover a sizable portion of the construction costs from the two subcontractors who are taking on liability for $10 million.

Table J: Accounting for Reimbursements from Subcontractors

(Source: Author)

Receipts due from subcontractors show how much money is expected to be reimbursed for the costs of their work. On the settlement entry, it shows the expected repayment as a gain because High Ltd thinks it will get back more than the newly recognised provision for bad construction.

It is necessary to know about these ideas before it can record liabilities like costs receivable and reimbursements receivable.

Recognition Criteria for Liabilities- A past event (in this case, construction defects) that will result in an outflow of economic benefits must have caused the probable Outflow of Resources, which is an obligation (Refer to case study). One can get an excellent grasp of how much the liability is.

Recognition of Provision- While there is a current obligation (whether constructive or formal) as a consequence of a previous occurrence and it is probable that an outflow of resources with economic benefits would be required to pay the obligation, a provision is mentioned (Refer to case study and evaluation).

Recognition of Receivables- Receivables from third parties, like the subcontractors in this case, are recorded when it is virtually certain that the inflow of economic benefits will result from a past event and when the exact amount of the receivable can be calculated.

Issue

The issue involves accurately accounting for the estimated costs to fix defects in a power plant construction project, altering the provision for defective subcontractors, and noting expected reimbursements from subcontractors (Alsalmi et al. 2023). It is challenging to accurately record these expenses and liabilities in accordance with base standards in order to ensure that receivables and liabilities are recorded based on the criteria for recognition of receivables and liabilities (Refer to case study).

Accounting treatments

In order to reflect the actual plant costs in this case, the provision for defects paid in the term power plant project needs to be changed. Use AASB 137 provisions, contingent liabilities, and contingent assets to determine the appropriate level of provision for the defects (AASB Standard, 2018). Increase the provision for defective subcontractors to cover the additional costs required beyond the original estimate. This must be taken into consideration, according to AASB 137 and AASB 116 (AASB Standard, 2018). Record expected reimbursements from subcontractors as accounts in accordance with AASB 15 Revenue from Contracts with Customers as long as it is virtually certain that the refund will be received (AASB Standard, 2018). For example, BHP Group accurately records provisions and liabilities for large-scale mining projects (BHP, 2023). They follow strict accounting standards that make sure financial reporting is clear.

According to Australian Accounting Standards, especially AASB 136, impairment of Assets, the ice cream factory's situation would be accounted for as follows.

Assessment for Impairment- The first step to take is to determine if there is any indication that the factory's net assets can be declining (AASB Standard, 2018). The estimated recoverable amount of $ 350M is less than the holding amounts of $400M, indicating a potential impairment in this case (Refer to case study).

Impairment Test- An impairment test should be given to find out how much term loss there is. The impairment loss is calculated from the discrepancy between the carrying amount and the recoverable amount.

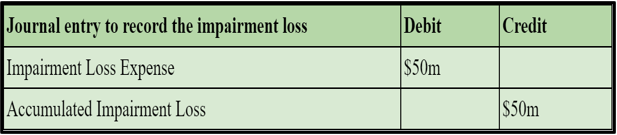

Recording the Impairment Loss- The $50 million loss due to impairment should be shown on the income statement as soon as it is found. It should be reported separately and be used to figure out the operating term or profit.

Table K: Journal entry to record the impairment loss

(Source: Author)

Subsequent Measurement- After impairment ($350M in this case), the assets' carrying value is changed to their recoverable value. While this business wants to spread the new carrying amount, minus any extra value, evenly over the asset's remaining useful life, they should change the depreciation or amortisation charges for it in later periods (AASB Standard, 2018).

Reversal of Impairment Loss- While there is an increase in the recoverable amount of the impairment loss in later periods, the impairment loss can be overturned (Refer to case study). Instead, only to the extent that the asset's carrying value is less than it would have been without the impairment loss.

For example, Qantas Airways Ltd. saw impairment losses on its fleet during the COVID-19 spread because fewer people wanted to travel, and there were limits on how many people could travel (QANTAS, 2021). That way, Qantas could accurately show how the recoverable amount of its assets went down. This was in line with AASB standards and made financial reporting easier to understand.

Explanation

The closure of the chocolate plant should be recorded in the financial statements of 2024 because it complies with the standards for recording under AASB 137 (AASB Standard, 2018). The decision to close the plant on March 18, 2024, the detailed plan that was agreed upon on can 25, 2024, and the actions that followed (letters sent to customers and redundancy notices to staff) all show that the company has a probable obligation to close the plant, which will result in a flow out of economic benefits (Refer to case study).

Issue

All that should be included in the financial statements as a provision for the plant's closure is the main long-term issue (Samson and Swink, 2023). This includes finding out the costs associated with the closure, such as staff move and retraining costs, term costs associated with selling a line of business, and term operating costs (Refer to case study). The profit from selling assets and paying off liabilities is less than the carrying value of the plant's net assets, so a provision for the difference needs to be made.

Treatment by Australian Accounting Standards

According to the "AASB," a company shall make provisions for any legal or constructive obligation resulting from a past occurrence (AASB Standard, 2018). A reliable estimate of the quantity of the debt may be created, and it is probable that an outflow of resources representing economic benefits will be required to pay off the debt. The board's decision and strategy give the company a constructive obligation to close the plant (AASB Standard, 2018). It is probable that an outflow of economic gains will be required to pay off the obligation given the costs of retraining, relocation, and operating (AASB Standard, 2018). Keep the provision amount equal to or more than the expenditure required to pay off the existing obligation at the end of the reporting month. The financial statements for 2024 should contain a provision for plant closure costs.

AASB Standard (2018) Property, plant and equipment. Available at: https://www.aasb.gov.au/admin/file/content105/c9/AASB116_08-15_COMPdec16_01-19.pdf (Accessed: 6th June 2024).

Alsalmi, N., Ullah, S. and Rafique, M., 2023. Accounting for digital currencies. Research in International Business and Finance, 64, p.101897.

BHP (2023) Natural capital accounting for the Mining Sector Beenup Site ... Available at: https://www.bhp.com/-/media/documents/environment/2023/230502_bhpbeenuppilotcasestudynaturalcapitalaccountingreport.pdf (Accessed: 7th June 2024).

Christensen, D., 2024. An Evaluation of the Informativeness of the Dual-Classification System for Leases. Available at SSRN 4712480.

Even-Tov, O., Ryans, J. and Solomon, S.D., 2024. Representations and warranties insurance in mergers and acquisitions. Review of Accounting Studies, 29(1), pp.423-450.

Harianto, A., 2023. The Analysis of Statement of Cash Flow in Assessing the Financial Performance at PT Akasha Wira International TBK. Jurnal Kolaboratif Sains, 6(7), pp.863-871.

Kartapanis, A. and Yust, C.G., 2024. Getting back to the source: A new approach to measuring ex ante litigation risk using plaintiff-lawyer views of SEC filings. Journal of Financial and Quantitative Analysis, 59(3), pp.1213-1256.

QANTAS (2021) Qantas Airways Limited and its controlled ... Available at: https://investor.qantas.com/FormBuilder/_Resource/_module/doLLG5ufYkCyEPjF1tpgyw/file/2022HY/1H22-Appendix-4D.pdf (Accessed: 11 June 2024).

Samson, D. and Swink, M., 2023. People, performance and transition: A case study of psychological contract and stakeholder orientation in the Toyota Australia plant closure. Journal of Operations Management, 69(1), pp.67-101.

Thathoba, P.C., 2023. The enforcement of settlement of agreements and arbitration awards.

Essay: 10 Pages, Deadline: 2 days

They delivered my assignment early. They also respond promptly. This is excellent. Tutors answer my questions professionally and courteously. Good job. Thanks!

![]() User ID: 9***95 United

States

User ID: 9***95 United

States

Report: 10 Pages, Deadline: 4 days

After sleeping for only a few hours a day for the entire week, I was very weary and lacked the motivation to write anything or think about any suggestions for the writer to include in the paper. I am glad I chose your service and was pleasantly pleased by the quality. The paper is complete and ready for submission to the professor. Thanks!

![]() User ID: 9***85 United

States

User ID: 9***85 United

States

Assignment: 8 Pages, Deadline: 3 days

I resorted to the MBA assignment Expert in the hopes that they would provide different outcomes after receiving unsatisfactory results from other assignment writing organizations, and they genuinely are fantastic! I received exactly what I was looking for from this writing service. I'm grateful.

![]() User ID: 9***55

User ID: 9***55

Assignment: 13 Pages, Deadline: 3 days

Incredible response! I could not believe I had received the completed assignment so far ahead of the deadline. Their expert team of writers effortlessly provided me with high-quality content. I only received an A because of their assistance. Thank you very much!

![]() User ID: 6***15 United

States

User ID: 6***15 United

States

Essay: 8 Pages, Deadline: 3 days

This expert work was very nice and clean.expert did the included more words which was very kind of them.Thank you for the service.

![]() User

ID: 9***95 United

States

User

ID: 9***95 United

States

Report: 15 Pages, Deadline: 5 days

Cheers on the excellent work, which involved asking questions to clarify anything they were unclear about and ensuring that any necessary adjustments were made promptly.

![]() User ID: 9***95 United

States

User ID: 9***95 United

States

Essay: 9 Pages, Deadline: 5 days

To be really honest, I can't bear writing essays or coursework. I'm fortunate to work with a writer who has always produced flawless work. What a wonderful and accessible service. Satisfied!

![]() User ID: 9***95

User ID: 9***95

Essay: 12 Pages, Deadline: 4 days

My essay submission to the university has never been so simple. As soon as I discovered this assignment helpline, however, everything improved. They offer assistance with all forms of academic assignments. The finest aspect is that there is also an option for escalation. We will get a solution on time.

![]() User ID: 9***95 United

States

User ID: 9***95 United

States

Essay: 15 Pages, Deadline: 3 days

This is my first experience with expert MBA assignment expert. They provide me with excellent service and complete my project within 48 hours before the deadline; I will attempt them again in the future.

![]() User ID: 9***95 United

States

User ID: 9***95 United

States